GST Regulations on Audit, Assessment and Adjudication – What’s the Ground Reality?

We’re seeing a broad adoption of the Goods and Services Tax and GST regulations in India as it gets closer to its sixth year of implementation among the government and taxpayers. Over time, GST regulations have progressively assimilated into a wide range of sectors, consulting firms, and other pertinent organizations.

Due to the complex nature of its GST regulations, taxpayers often encounter issues in their daily business that require immediate attention. For example, a GST audit, adjudication notice under the GST, and GST assessments typically make a company feel incredibly uneasy, akin to a raid. However, let’s examine how manageable these situations actually are.

This article aims to give a general overview of the assessment, adjudication, and recovery framework described in the Central Goods and Services Tax Act, 2017 (CGST Act), as well as to outline potential problems that taxpayers may encounter.

Adjudication Notice under GST:

An adjudication notice under GST regulations represents a formal communication from the GST department directed at a registered individual who has breached or failed to comply with GST regulations. Adjudication notice under GST regulations is issued in accordance with Sections 73 and 74 of the CGST Act, 2017; this adjudication notice under GST provides the registered person with a chance to present their side and address the accusations made by the Adjudication authority under GST.

The scrutiny assessment, outlined in section 60 of the CGST Act, involves a meticulous review of filed returns to identify discrepancies and inconsistencies, followed by the issuance of an online notice.

Common Reasons For Receiving an Adjudication Notice under GST

· Discrepancies in tax liabilities reported between GSTR-1 and GSTR-3B.

· Variances in Input Tax Credit between GSTR-3B and GSTR-2B.

· Imposition of interest due to delayed filing of GSTR-3B returns, resulting in delayed tax payment. The interest is confined to the net tax liability settled in cash.

· Discrepancies in E-way Bills related to outward supplies concerning GSTR-1.

· Inconsistencies in E-way Bills associated with inward supplies in contrast to GSTR-3B.

Tax Authority Audit:

The tax authority’s audit, as per section 65 of the CGST Act/State Act, commences with issuing a notice in Form GST ADT-01. This audit, covering a span of three years from 2017 to 2020, was conducted by authorities outside the jurisdictional circle. Initial documents requested include:

- Audited financial statements.

- Tax audit reports.

- Cost audit reports.

- Independent auditors’ reports.

- Other registers.

- Returns.

- Supporting documentation.

For manufacturing industries, a questionnaire focusing on internal controls and procedures is also gathered.

The initial phase of the Department’s audit targets exporters claiming refunds and suppliers dealing with risky exporters. The notice issuance extended from the end of 2020 well into 2021, coinciding with the government’s efforts to identify and address legal pitfalls and loopholes. In our vast economy, the emergence and disappearance of fraudulent entities are not uncommon. However, genuine taxpayers have borne the burden of revenue disparities in the pursuit of eliminating these entities.

Crucial aspects in demand provisions:

The GST law showcases an initial divergence from its predecessor, the service tax law, by segregating cases involving fraud and normal cases into distinct sections. Unlike the service tax laws, which had a single section covering these scenarios, the GST regulations separate these issues into Section 73 and Section 74, respectively.

In the service tax laws, Section 73 focused solely on issuing Show Cause Notices (SCN) related to service tax, while matters concerning input tax credit were governed by Rule 14 of the CENVAT Credit Rules, 2004. However, under GST, Section 73 encompasses instances of wrongly availed or utilized input tax credits as well.

Additionally, Section 75 (10) of the CGST Act 2017 stipulates a deemed conclusion of adjudication proceedings if an order isn’t issued within 3 or 5 years. Though similar provisions existed in service tax laws, the language was more open-ended, using the phrase ‘where it is possible to do so.’

The GST regulations primarily rely on the annual return GSTR-9 as the determining factor for setting the time limit for order issuance. However, this creates ambiguity, particularly for causal taxable persons and non-residents who don’t file annual returns. It raises the question of the time limit for issuing orders in such cases.

Regarding cases where amounts are collected but remain unpaid, unlike the service tax regime, Section 76 of the CGST Act 2017 doesn’t specify any time limit for SCN issuance.

Furthermore, in instances where an SCN issued under Section 74 due to fraud is deemed unsustainable, the tax payable shifts to Section 73. This results in the reduction of the alleged demand period from 5 years to 3 years automatically.

Timeline for Show Cause Notice (SCN) and Concluding Adjudication:

The CGST Act of 2017 covers a range of audits and assessments. However, only some evaluations or audits result in the CGST Act, 2017’s Sections 73 and 74, which require issuing a show cause notice (SCN). For instance, in assessments of non-filers of returns or unregistered persons, the assessment can conclude without the necessity of an SCN under Section 73/74. The provisions for issuing notices and concluding assessments are separately addressed in the respective sections for such cases.

Under the CGST Act 2017, the issuance of SCN under Section 73/74 typically occurs in cases involving return scrutiny, summary assessment, tax authority audits, or special audits. Regardless, it’s crucial to note that tax officers can conduct assessments or audits within a maximum period of 5 years from the date of filing annual returns for a specific year.

In contrast, under the service tax laws, the SCN must be issued by 2.5 years/5 years from the due date of filing service tax returns in Form ST-3. For example, if the due date for the ST-3 period from April 2017 to June 2017 were August 15, 2017, the SCN’s maximum issuance period would be:

Normal cases: Within 2.5 years, i.e., on or before February 15, 2020

Cases involving fraud, etc.: Within 5 years, i.e., on or before August 15, 2022

Moreover, while the service tax law lacks specific timelines for concluding adjudication proceedings, higher courts have consistently indicated that adjudication should ideally be completed within 5 years from the date of the SCN.

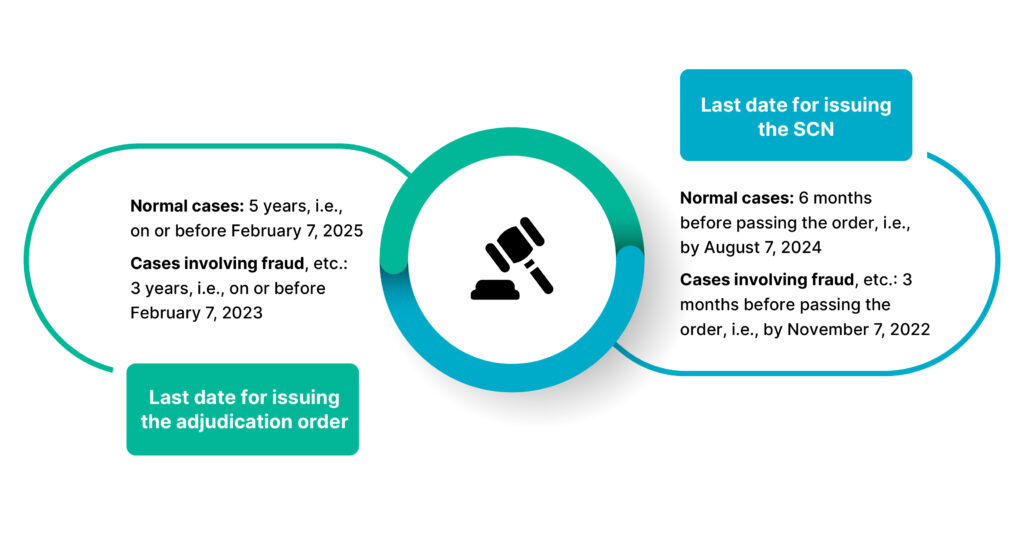

Limitation Periods under GST Law for GST Audit:

Under the GST regulations, the limitation periods are as follows for the financial year 2017-18:

GST regulations after adjudication notice under GST:

Aside from outlining detailed assessment, adjudication, and appeal procedures, the CGST Act includes provisions for the direct recovery of owed amounts from taxpayers at different junctures. Section 78 of the CGST Act enables the initiation of recovery proceedings following any order under the act if the taxpayer fails to settle the demand within three months of the order’s service. This timeline aligns with the three-month limit for filing an appeal.

However, a provision within Section 78 allows a proper officer, in the ‘interest of revenue,’ to demand payment even before the expiry of these three months. Similarly, Section 83 permits provisional property attachment in the ‘interest of revenue.’ Yet, what defines ‘interest of revenue’ or what deems such interest ‘expedient needs’ is a specific definition or qualification within the act or rules. This underscores the necessity for a departmental circular or guideline elucidating the scope of these terms.

The GST regulations offer various modes of recovery to the adjudicating authority under GST, including bank attachment, sale of assets, encashment of bonds, detention and sale of goods, adjusting or withholding sanctioned refunds and debiting from electronic cash or credit ledgers.

These recovery mechanisms aren’t solely applicable when demands are confirmed through orders. They also come into play when tax liabilities are self-assessed through filed returns or when interest or late fees remain unpaid due to return filing delays, among other scenarios.

In summary, the adjudicating authority under GST possesses multiple avenues to recover tax dues deemed ‘expedient in the interest of revenue’ based on their discretion and judgment.

Way Ahead For Businesses and Taxpayers:

To sum up, an adjudication notice under GST regulations signifies a formal notification from the adjudicating authority under GST directed at a registered entity that breaches GST regulations. Businesses must comprehend the legal framework surrounding these notices and their proper handling. Disregarding an adjudication notice can result in severe repercussions like penalties, interest charges, and potential legal action. To avert receiving such notices, businesses must uphold precise records and adhere meticulously to GST regulations.